A Comparative Study On Merger

We are living in a free market economy age where business entities are engaged

in practicing competition. Sometimes it leads to the monopolization of market by

way of anti-competitive agreements, abuse of dominance, mergers and takeovers

between business entities which results in distortion of market.

Most countries in the world have enacted competition laws to protect their free market economies and have thereby developed an economic system in which the allocation of resources is determined solely by demand and supply. In the case of India, the earlier Monopolies and Restrictive Trade Practices Act, 1969 (MRTP) was not only found to be inadequate but also obsolete in certain respects, particularly, in the light of such international economic developments relating to competition law.

To overcome such difficulty Indian Government has enacted the Competition Act in 2002. This enactment is seen as India's response to the opening up of its economy, removing controls and resorting to liberalization. The Act sought to ensure fair competition in India by prohibiting trade practices which cause appreciable adverse effect on the competition in market within India.

The present Indian Act is quite contemporary to the laws presently in force in the European Community as well as in the United Kingdom or in any other jurisdictions. In other words, the laws dealing with competition in these jurisdictions have somewhat similar legislative intent and scheme of enforcement.

We are living in a free market economy age where business entities are engaged in practicing competition. Sometimes it leads to the monopolization of market by way of anti-competitive agreements, abuse of dominance, mergers and takeovers between business entities which results in distortion of market. Most countries in the world have enacted competition laws to protect their free market economies and have thereby developed an economic system in which the allocation of resources is determined solely by demand and supply.

In the case of India, the earlier Monopolies and Restrictive Trade Practices Act, 1969 (MRTP) was not only found to be inadequate but also obsolete in certain respects, particularly, in the light of such international economic developments relating to competition law. To overcome such difficulty Indian Government has enacted the Competition Act in 2002. This enactment is seen as India's response to the opening up of its economy, removing controls and resorting to liberalization.

The Act sought to ensure fair competition in India by prohibiting trade practices which cause appreciable adverse effect on the competition in market within India. The present Indian Act is quite contemporary to the laws presently in force in the European Community as well as in the United Kingdom or in any other jurisdictions. In other words, the laws dealing with competition in these jurisdictions have somewhat similar legislative intent and scheme of enforcement.

Historical background of merger

The concept of merger and acquisition in India was not popular until the year 1988. During that period a very small percentage of businesses in the country used to come together, mostly into a friendly acquisition with a negotiated deal. The key factor contributing to fewer companies involved in the merger was the regulatory and prohibitory provisions of MRTP Act, 1969. According to this Act, a company or a firm has to follow a burdensome procedure to get approval for merger and acquisitions.

The year 1988 witnessed one of the oldest business acquisitions or company mergers attempt in India.

It is the well-known ineffective unfriendly takeover bid by Swaraj Paul to overpower DCM Ltd. and Escorts Ltd. Further to that many other non-resident Indians had put in their efforts to take control over various companies through their stock exchange portfolio.

Before 1991 Indian economy was closed economy. Various licenses and registration under various enactments were required to set-up an industry. Due to restrictive government policies and rigid regulatory framework there existed very limited scope for restructuring.

However after 1991, the main thrust of industrial policy 1991, was on relaxations in industrial licensing, foreign investments, and transfer of foreign technology, etc. With the economic liberalization, globalization and opening-up of economies, the Indian corporate sector started restructuring businesses to meet the opportunities and challenges.

Regulatory approval of schemes

Combination (Section 5 of Competition Act, 2002)

The Competition Act 2002 is the principal legislation that regulates combinations (acquisitions, mergers, amalgamations and de-mergers) in India. Sections 5 and 6 of the Competition Act, which deal with the regulation of combinations, have been in force since 1st June 2011. Prior to this date there was no statutory obligation to notify to any antitrust authority before completing merger and amalgamations. Section 5 of the Act prescribes the jurisdictional thresholds limits (based on asset and turnover of combining companies) for transactions that must be notified to CCI prior to implementation of merger and acquisition.

Meaning of combination for the purpose of Competition Act

Regulatory Authority for Notifying Combinations- The Competition Commission of India (CCI) is the statutory authority responsible for reviewing combinations and assessing whether or not they cause or are likely to cause an appreciable adverse effect on competition within the relevant market(s) in India. CCI approval is required for combinations where the parties involved exceed the assets/turnover thresholds set out in section 5 of the Competition Act.

Exemption from provision of Combination

The Central govt. has granted exemption from application of section 5 or Section 6:

Types of notifiable transactions:

Section 5 of the Competition Act, 2002 covers three broad categories of combinations:

Taxation aspects of Merger and Amalgamation

The word 'amalgamation' or 'merger' is not defined anywhere in the Companies Act, 1956. However, the Companies Act, 2013 without strictly defining the term explains the concept. A 'merger' is a combination of two or more entities into one; the desired effect being not just the accumulation of assets and liabilities of the distinct entities, but organization of such entity into one business. Section 2(1B) of the Income Tax Act, 1961 defines the term 'amalgamation' as follows:

"Amalgamation" in relation to companies, means the merger of one or more companies with another company or the merger of two or more companies to form one company (the company or

companies which so merge being referred to as the amalgamating company or companies and the company with which they merge or which is formed as a result of the merger, as the amalgamated company), in such a manner that:

Stamp duty aspects of Merger and Amalgamation:

Federal Trade Commission (FTC) - United States:

In the United States, the FTC, along with the Department of Justice, enforces antitrust laws, including the Hart-Scott-Rodino (HSR) Act. Among the key provisions in U.S. antitrust law is one designed to prevent anticompetitive mergers or acquisitions. Under the Hart-Scott-Rodino Act, the FTC and the Department of Justice review most of the proposed transactions that affect commerce in the United States and are over a certain size, and either agency can take legal action to block deals that it believes would "substantially lessen competition." Although there are some exemptions, for the most part current law requires companies to report any deal that is valued at more than $101 million to the agencies so they can be reviewed.

Steps in the Merger Review Process:

Clearance to one antitrust agency:

Parties proposing a deal file with both the FTC and DOJ, but only one antitrust agency will review the proposed merger. Staffs from the FTC and DOJ consult and the matter is "cleared" to one agency or the other for review (this is known as the "clearance process"). Once clearance is granted, the investigating agency can obtain non-public information from various sources, including the parties to the deal or other industry participants.

Waiting period expires or agency issued second notice

After a preliminary review of the premerger filing, the agency can:

Typically, once both companies have substantially complied with the Second Request, the agency has an additional 30 days to review the materials and take action, if necessary. (In the case of a cash tender offer or bankruptcy, the agency has 10 days to complete its review and the time begins to run as soon as the buyer has substantially complied.) The length of time for this phase of review may be extended by agreement between the parties and the government in an effort to resolve any remaining issues without litigation.

The FTC conducts a thorough investigation to determine if the merger would substantially lessen competition. Factors Considered:

The FTC considers market concentration, entry barriers, potential efficiencies, and other factors to assess competitive impact Remedies:

The FTC may seek remedies, such as divestitures or behavioral remedies, to address anticompetitive concerns.

EUROPEAN UNION:

The development of merger control in the European Union

The European Union ("the EU") is a regional grouping of (at the time of writing) 25 European States. It is based on a number of international treaties of which the most important, for present purposes, is the Treaty establishing the European Community ("the EC Treaty"). The Member States of the European Community (the EC) are the same as the Member States of the EU. The difference between the EU and the EC is largely technical and not relevant in the present context. No specific provision is made for the control of mergers in the EC Treaty.

The main competition rules contained in the Treaty, Articles 81 and 82 EC, are primarily directed at controlling the conduct of firms (or "undertakings") rather than at changes to the structure of the market. Neither explicitly mentions mergers. Despite the creative interpretation of Articles 81 and 82 EC, which extended their application to at least some merger activity, it was apparent from an early stage in the EC's development that legislation would be needed in order to institute an effective system of merger control.

The Commission of the European Communities ("the Commission") first proposed a regulation on the subject in 1973. It was not until 1989, however, that agreement could finally be reached among the Member States. The result was the adoption of Council Regulation (EEC) No. 4064/89, which was subsequently amended in 1997, and was replaced in 2004 by a new Regulation No. 139/2004, further modifying and consolidating the EC system of merger control.

The attempt to use Articles 81 and 82 EC to control mergers

In a memorandum issued in 1966, the Commission adopted the position that Article 81 EC did not apply at all to agreements "whose purpose is the acquisition of total or partial ownership of enterprises". That article prohibits agreements between undertakings which have as their object or effect to prevent, restrict or distort competition. The commission considered that it would only apply to an agreement between undertakings which remained independent of one another, which would not be the case if the agreement resulted in full merger.

The original EC merger regulation

The Council adopted the original EC merger control regulation on 21 December 1989. It entered into force on 21 September 1990. The system of merger control which it instituted still retains the same basic structure, despite its subsequent amendment and ultimate replacement.

That system applies to "concentrations" having a "Community dimension". Mergers not meeting those jurisdictional criteria fall, in most cases, to be considered under any applicable national merger control rules. Those mergers which meet the criteria are, in most cases, subject to exclusive control at the EC level (under the so-called "one-stop-shop principle").

However, the division thus established between national and EC merger regimes has from the outset been subject to a system of "referrals", allowing for mergers not meeting the jurisdictional criteria to be "referred up" by national authorities to be dealt with by the Commission under the EC rules, or for mergers meeting those criteria to be wholly or partially "referred down" by the Commission to national authorities for control under national law. The circumstances in which such referral may take place have been extended with effect from May 2004.

Mergers to which the EC rules apply are subject to compulsory pre-notification. They must be notified to the Commission, and may not be put into effect until the Commission has reached a decision upon them.

Under the substantive test contained in the original EC merger control regulation, a merger would be incompatible with the common market, and therefore prohibited, if it "created or strengthened a dominant position as a result of which effective competition would be significantly impeded in the common market or in a substantial part of it". As explained below, 18 that test have recently been amended.

Thresholds:

Mergers with an EU dimension (i.e., affecting multiple EU member states) and meeting certain turnover thresholds must be notified to the EC.

STEPS IN MERGER REVIEW PROCESS:

Phase II Investigation

Phase II is an in-depth analysis of the merger's effects on competition and requires more time. A Phase II investigation is opened when the case cannot be resolved in Phase I. From the opening of a Phase II investigation, the Commission has 90 working days to make a final decision on the compatibility of the planned transaction with the EU Merger Regulation. Extensions of either 15 or 20 working days can be granted.

Remedies

If the Commission has concerns that the merger may significantly affect competition, the merging companies may offer remedies ("commitments"), i.e. propose certain modifications to the project that would guarantee continued competition on the market. Companies may offer remedies in phase I or in phase II.

The final decision

Following the phase II investigation, the Commission may either

A residual role for Articles 81 and 82 EC

Recital 19 of the Merger Regulation confirms that the exclusive application of the Regulation to concentrations with a Community dimension is without prejudice to Article 296 of the Treaty. Under Article 296(1)(b), a "Member State may take such measures as it considers necessary for the protection of the essential interests of its security which are connected with the production of or trade in arms, munitions and war material" provided that such measures do not adversely affect the conditions of competition in the common market regarding products which are not intended for specifically military purposes.

Where Article 296(1)(b) EC is successfully invoked, the Commission considers the impact of the merger only in relation to goods and services which are exclusively "civilian" in character, or which are "dual use", serving both a military and a non-military function. Exclusively military aspects are not notified to the Commission at the instruction of the Member State whose defence industry is at stake.

BRAZIL:

Relevant legislation and statutory standards

The first Brazilian law specifically dealing with competition issues was Law 4137 of 10 September 1962, containing general rules on abuse of economic power, with broad and generic provisions aimed at controlling acts and contracts that could harm competition on the Brazilian market. This law created the Administrative Council for Economic Defence (Conselho Admin istrativo de Defesa Economica - "CADE"), the Brazilian authority charged with enforcing the competition law. Other laws and decrees of lesser importance were subsequently issued, also dealing with this matter.

However, as the national economy was strongly closed, suffering a rigid control of prices set by the Federal Government, the enforcement of these legal provisions was minimal and the competition culture almost null. On a parallel basis, and also as a result of the legal environment, the local business community was not familiar with competition rules, mainly due to the country's political and economic history where governmental control over most economic sectors and industries had been the ground rule for decades.

It was only in the mid-1990s that the current Brazilian competition law was enacted, in a moment when the country was undergoing a significant number of privatizations, the outset of currency stabilization, and the gradual opening of the national economy. It was within this context, on 11 June 1994, that the Brazilian Competition Act (Law 8884/94) was enacted with the main purpose of developing and improving competition defence in Brazil to cope with the beginning of this new market reality.

Essentially, the Competition Act made competition law control and enforcement a reality in Brazil. It changed CADE into a federal independent agency reporting to the Ministry of Justice. With specifically defined and enhanced powers to monitor and curb potential abuses of economic power.

The Competition Act is firmly grounded on the Federal Constitution of 1988 and is guided by the constitutional principles of free enterprise, open competition, consumer rights protection, the social purpose of property, and restraint of unfair trade practices and abuses of economic power. These constitutional principles equally provide the general guidelines for economic activities, as set forth in Sections 170 et seq. of the Federal Constitution."

As usually occurs in young jurisdictions, the legislators drafted the Competition Act essentially based on concepts and provisions contained in foreign competition legislation, especially the US antitrust law (the Sherman and Clayton Acts) as well as on the Treaty of Rome applying to the European Union (EU).

The Competition Act applies to acts fully or partially performed within the Brazilian territory, as well as to acts undertaken abroad with actual or potential effects on the Brazilian market, but without prejudice to treaties to which Brazil is a party. For purposes of the Competition Act, any foreign company that operates or has a branch, agency or office, establishment, agent or representative in Brazil is located in Brazil.

In general terms, the Competition Act protects competition in basically two ways:

Through preventive measures to control acts and contracts that may lead to an abusive economic concentration or to abusive exercise of a dominant position, pursuant to its Section 54 (merger control).

Through restrictive measures to curb potentially anti-competitive practices, pursuant to its Sections 20 and 21 (control of restraints of trade).

Thresholds

Mergers meeting certain revenue thresholds require mandatory notification to CADE.

Procedures and formalities for the notification

Once it is determined that an act or contract meets the thresholds established by law, the parties must then observe the procedures and formalities concerning the documentation to be submitted to CADE, SDE and SEAE, as presently set forth in Resolution 15/98.

For a competition law filing in Brazil, the parties to any type of transaction must fill out a specific and standard form. This form appears as the Attachment I to Resolution 15/98 (the "CADE form"), which must be fully and jointly completed by the reporting parties. Accordingly, for each transaction one single filing is required, to be made jointly by the parties to the deal. The CADE form is basically divided into six sections, as follows:

Part I - The petitioner: The first part of the CADE form refers to data on the notifying parties ("petitioners"), which are usually those involved in the deal, that is the entities executing the 16 corresponding agreement. This part contains detailed institutional/corporate information on the companies, such as the names of their principal shareholders or partners; a description of the business carried out by the parties and by their economic groups worldwide.

Part II - The act or agreement under notification: The act or agreement under notification. This part seeks to define, in each specific case, the economic transaction submitted to SBDC. Essentially, the information refers to the structure, date and value involved in the transaction (as per the underlying agreements), and the parties' reasons for entering into the transaction.

As it is the main object of review, the agreement providing for the transaction must be clearly explained to the competition authorities.

Part III- The documentation: Another part of the CADE form refers to the documents required for submission of the economic transaction to SBDC, which basically comprise:

The purpose is for the competition authorities to be able to identify whether there is any kind of overlapping business among the companies involved in the transaction (horizontal relationship) and/or any vertical integration among them (relationship along the production chain). If there is any actual or potential horizontal relation and vertical integration among the parties to the transaction in Brazil, the next step of the competition authorities will be to verify the effects of these relations on the market from a competition perspective.

Part V - Relevant markets and Part VI - General conditions in the relevant markets: These parts of the CADE form are the key points of any competition law review, in that they refer to the so called "relevant markets" and there main features. In these parts the companies are required to define the relevant market affected by the economic transaction under review, meaning the one in which the competition between the parties will actually occur.

To summarize, it is therefore essential to complete the CADE form fully and correctly with the information and data described above in order to ensure a proper and efficient review of the transaction. The authorities in charge of the case, at their discretion and depending mainly on the complexity of the transaction from the competition viewpoint, may request additional clarification and information of the parties and also of third parties (such as customers/suppliers/competitors).

It should be noted that such request stop the clock on deadlines that the authorities must comply with and it is accordingly in the interest of parties to reply promptly to ensure a swift resolution of their case.

Upon filing a case before CADE, the petitioners must comply with the payment of a filing fee of R $45,000, which currently corresponds to roughly US $15,000.18 It is worth mentioning that such value applies irrespective of the type and size of transactions.

Timing for the notification

As for timing, the Competition Act, in its section 54(4), determines that a reportable transaction should be presented "previously or within a maximum period of fifteen business days after its occurrence." The Competition Act does not formally define what the "occurrence" of a transaction is, and for this reason it is often quite difficult to know precisely which is the triggering event for a competition filing in Brazil.

In fact, the wording of the law and the lack of a formal and direct guidance of the authorities with regards to this issue generate confusion as to when the 15 business day period should start and have resulted in a high number of fines being imposed on companies for late notification to CADE.

Co-operation Agreement between the USA and Brazil

Despite the challenges and shortcomings involved, it is indisputable that bilateral agreements based on the principles of positive comity serve as an effective tool for harmonisation of the competition systems across several jurisdictions.

Accordingly, the agreement between the Brazilian Government and the Government of the USA provides for co-operation between the countries' respective competition authorities in the enforcement of competition laws.

This specific agreement was signed by both Governments on 26 October 1999, but was approved by the Brazilian Government only in March 2003.55 Its great importance derives from the fact that a vast array of deals filed with the Brazilian competition authorities have originally been structured abroad and are submitted for CADE's review because of their impact on the Brazilian market. Based on publicly available information, out of the deals notified to Brazilian competition authorities: roughly 65% were thoroughly structured between foreign companies abroad; roughly 17% referred to deals among foreign and Brazilian companies; and only 18% referred to exclusively Brazilian deals.

The merit of agreements of this ilk is to promote co-operation and co- ordination between the competition authorities in each country to increase the effectiveness of each party's competition law enforcement efforts as well as to avoid conflicts from the application of competition laws. As it is publicly known, the USA had already signed similar agreements with the EU, Canada, Germany, Australia, Israel and Japan.

CHINA

Relevant legislation and statutory standards

Mergers and acquisitions in China are currently subject to a variety of laws and regulations.

These include the following:

Steps in merger review process:

Decision making

So far, the most comprehensive merger and acquisition regulations in China (and consequently the focus of this chapter) are the Interim Provisions on "M&A Rules", which were issued jointly by the Ministry of Commerce ("MOC/MOFCOM"), the State Administration for Industry and Commerce (SAIC), the State Administration of Taxation (SAT) and the State Administration of Foreign Exchange ("SAFE").

The MOC and SAIC are jointly responsible for administering the M&A Rules, which cover "mergers with and acquisitions of domestic enterprises by foreign investors". Although these provisions therefore only apply to transactions involving foreign parties, the M&A Rules cover both onshore and offshore transactions in circumstances set out below.

Onshore transactions

Onshore transactions covered by the M&A Rules include mergers and acquisitions effected both by equity investments and asset purchases involving foreign investors and Chinese enterprises ("domestic enterprises") with no previous foreign investment.

"Equity Mergers and Acquisitions" arise either where the foreign investor purchases an equity interest in a domestic enterprise from existing investors or subscribes to an increase in the registered capital of that domestic company. Such transactions result in the domestic enterprise being converted into a foreign investment enterprise ("FIE").3 The M&A Rules also cover any direct acquisitions by foreign investors of equity interests in existing FIEs.

"Asset Mergers and Acquisitions," on the other hand, take place either where the foreign investor creates an FIE for the purpose of acquiring (through a purchase agreement) assets of a domestic enterprise which it will then manage; or where the investor directly purchases the assets in order to set up an FIE which will manage the acquired assets. Accordingly, a joint venture to set up a new FIE, whether between a foreign and domestic investor or several foreign investors, will be beyond the purview of the M&A Rules so long as it is not used as a vehicle to acquire or manage domestic assets.

The position is unclear where there is an onshore merger of existing FIEs. It is possible that such a case will come within the review mechanism under the M&A Rules procedures, but no clear answer has yet been given to this question. Article 3 merely stipulates that "foreign investors shall comply with laws, administrative regulations and departmental rules and adhere to principles of fairness, reasonableness, compensation for equal value and honesty and good faith, and shall not create excessive concentration, eliminate or hinder competition, disturb the social economic order or harm the societal public interests".

Offshore transactions

Whilst onshore transactions are automatically caught as the assessment process is tied up in other regulatory structures, the M&A Rules can also cover offshore transactions if the parties or any associated enterprises hold certain assets or operate a business in China, even where no PRC- registered entity is directly or ultimately involved.

Offshore joint ventures that satisfy the criteria of a merger or acquisition would be covered by the M&A Rules, although the Rules do not currently apply to joint ventures between domestic firms.

Remedies: The SAMR may impose remedies, such as divestitures or behavioral commitments, to address competition concerns.

It's important to note that merger review provisions and processes in these jurisdictions can evolve over time, and specific details may change. Consulting the respective competition authorities or legal experts for up-to-date information is recommended.

GUN JUMPING

INDIA

Gun jumping means acting before the right time and refers to situation where a party or parties to a combination consummate a transaction wholly or partially before the approval of CCI, thereby violating standstill obligations. All the combinations above the threshold limit specified by the commission and the combination cannot be consummated until approved by the commission.

Section 6(2) of the act places the obligation on the parties to give notice to the commission disclosing the details of the proposed combination.

Proceeding under section 43A of the Act

If the commission found a prima facie opinion that the combination is not notified prior to the consummation, the commission will issue a show cause notice under section 43A of the Act read with Regulation 48 of General Regulations. The parties provide their response to the notice and seek opportunity to provide its oral submission. The Commission fixes a date of hearing of the parties for the same. After completion of the hearing, the Commission passes an appropriate order, including the decision on the matter of imposition of penalty, based on the facts and circumstances of the case.

Penalties imposed under section 43 of the Act

Under Section 43A of the Act, the penalty may extend to one per cent (1%) of the total turnover or the assets, whichever is higher, of such a combination.

UNITED STATES AND EUROPEAN UNION

Both the US and the EU impose on parties to merger and acquisition transactions notification requirements when certain thresholds are met. The purpose of these requirements is to ensure that competition authorities have the opportunity to review transactions that could substantially harm competition before they are closed.

Gun jumping relates to unlawful pre-merger co-ordination between the parties to an M&A transaction. More precisely, it is a term used to describe two types of scenarios.

This type of conduct is generally prohibited in the US under section 1 of the Sherman Act and in the EU under Article 101 TFEU

Procedural Gun Jumping

Procedural gun jumping occurs when parties fail to notify the competition authorities of a transaction triggering merger thresholds, and where they implement a notifiable transaction without observing mandatory applicable waiting period and/or clearance requirements under relevant merger control laws. Procedural gun jumping refers to matters of control such as the premature combining of parties.

This type of conduct is prohibited under section 7A of the Clayton Act, the Hart-Scott Rodino Antitrust Improvements Act of 1976, as amended (HSR Act) and under Article 7(1) of the EU Merger Regulation.

Implications and consequences of breaching gun jumping laws:

UNITED STATES

In the US, even though enforcement actions involving gun jumping can be brought under both the HSR and the Sherman Act, they are often brought under the former. Violations of gun jumping provisions may be subject to fines of up to US$40,654 per day of violation, injunctive relief such as requiring the parties to implement an antitrust compliance programme, and disgorgement of any illegally obtained profits stemming from the violation.

EUROPEAN UNION

The Commission has used its power under the EU Merger Regulation to conduct dawn raids at the premises of merging parties (under Article 13 of the EU Merger Regulation) in order to determine whether exchanges of sensitive information had occurred in violation of the gun jumping provision.

The Commission can also prohibit the transaction altogether and require it to be unwound, and impose fines. Under Article 14(2) (b) of the EU Merger Regulation, the Commission can impose

fines up to 10% of the aggregate turnover of the undertakings concerned in the preceding financial year, as well as interim measures for the violation of the standstill obligation, irrespective of whether the infringement was committed negligently or intentionally and despite the fact that clearance might be ultimately obtained.

CHINA

According to the Anti-Monopoly Law of the People's Republic of China ("AML"), the Interim Provisions on the Examination of Concentrations of Undertakings and other relevant legal provisions, when a concentration of undertakings (including the establishment of joint ventures, share acquisition, etc.) reaches the filing thresholds, relevant parties to such concentrations are obliged to file pre-merger notification with China's antitrust regulator, the State Administration for Market Regulation (SAMR), and no concentration will be allowed without clearance from the SAMR during the review by SAMR, even if such filing has been carried out. The antitrust regulatory mechanisms in most of other major jurisdictions (such as the U.S. and the EU) adopt the ex-ante filing mechanism similar to what China applies to mitigate adverse impacts on market competition.

Under the ex-ante filing mechanism, if before receiving clearance from the antitrust regulator, the parties to a concentration implement, or fail to file, a concentration, such concentration may be deemed to constitute "gun-jumping" in violation of antitrust regulatory provisions and thereby may be subject to fines and other penalties with a view to restoring the parties to their pre-concentration status, and such penalties could be as serious as a halt concentration order and an order for the parties to take measures such as disposal of shares or assets and transfer of their business within a time limit.

Gun-jumping" is generally considered to fall into the following two patterns:

"Gun-jumping in Relation to Implementation of Concentrations without Filing as Required"

"Gun-jumping in Relation to Implementation of Concentrations before Receiving Clearance"

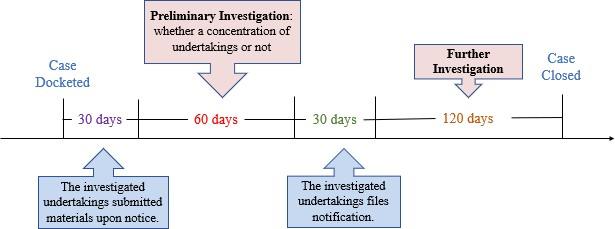

According to our preliminary research on all 50 sanction decisions on Gun-jumping Cases publicly available, 27 out of the 32 sanction decisions issued before 2019 revealed the date when the cases were docketed. By calculating the time intervals between the case docketing and the date of the decision, we could see it takes 244 days on average to close an investigation against Gun-jumping Case, ranging from 56 days to 465 days.

Figure: Timeline of investigations on gum jumping cases

In accordance with Article 48 of the AML, the upper limit of the fine is 500,000 Yuan for Gun- jumping Cases. In addition to that, the anti-monopoly law enforcement agency may also "order the cessation of concentration, disposal of the relevant equity or assets within the prescribed time limit, transfer of business within the prescribed time limit, and take other necessary measures to restore the pre-concentration status" which, however, has never been imposed in a real case.

In terms of the amount of fine for Gun-jumping Cases, we found most of the imposed fine was around CNY 150,000 to 200,000 in the cases investigated before April 2018. However, when it comes to 2019, the fines imposed go up to around CNY 300,000 to 400,000, except for the acquisition of Inad by Yinli Media in which Yinli Media was fined only CNY 200,000. By observing the trend of fines imposed in all investigated Gun-jumping Cases, it seems that the average amount of fine applied for Gun-jumping Cases is on the rise.

UNITED KINGDOM

On 24 September 2019 the UK Competition and Markets Authority ("CMA") imposed a fine of

�250,000 on PayPal, the California-headquartered supplier of payment services, for implementing its acquisition of iZettle in breach of an interim enforcement order ("IEO") which prohibited the integration of the parties' businesses pending the CMA's merger review. The fine is the largest ever imposed by the CMA for a single breach of an IEO.

STANDSTILL OBLIGATION

In the context of mergers, a standstill obligation refers to a requirement imposed by competition authorities or regulators that parties to a proposed merger must refrain from implementing the transaction until it has been reviewed and cleared by the appropriate authority. This obligation is

aimed at preventing potential harm to competition or other negative effects that could arise from a merger before it is fully assessed.

INDIA

The combination regulation regime in India is mandatory and suspensory. Section 6(2) of the Act imposes a standstill obligation on parties, i.e., parties must not give effect to the combination or any part thereof, before an order under Section 31 of the Act has been passed by CCI or until expiry of 210 days from the date of giving notice to CCI, whichever is earlier.

Purpose and objective of standstill obligation

Section 6(2A) of the Act, relating to standstill obligations, imposes a restriction upon the parties from consummating the proposed combination (even part-consummation is not allowed).

"The basic objective of standstill obligations contained in Section 6(2A) of the Act is to ensure that the parties to a combination transaction compete as they were competing before the initiation of combination process till the time the transaction is reviewed for any appreciable adverse effect on competition ("AAEC") and approved by the Commission. In other words, the standstill obligations essentially require that the parties carry on with their ordinary course activities completely independent of each other and to the fact of the combination transaction.

The objective of standstill obligations is to ensure that the parties remain independent competitors as they were before the proposed transaction, and accordingly, what constitutes contravention of standstill obligations is the activities, actions and arrangements, etc., which may reduce or have the potential to reduce the degree of independence or the incentives of the parties to compete as they were competing earlier.

Any action in furtherance of the transaction, including sharing of commercially sensitive information before such approval is granted, is likely to be seen as an instance of violating standstill obligations and may attract penalties under the Act.

Given that most transactions, especially mergers/amalgamations, require a pre-transaction due diligence, as well as a certain level of post-signing integration planning, parties need to be extremely cautious that such actions are not seen violating standstill obligations under Section 6(2A).

EUROPEAN UNION

The standstill obligation is laid down in Article 7(1) of the Merger Regulation which provides that a merger with a Community dimension may not be implemented until it has been declared compatible with the common market by a Commission decision or, in the absence of a decision, by expiry of the legal deadline. The standstill obligation also applies to public bids, since although

the acquisition of shares is allowed, the acquirer is required to notify the concentration without delay and must not exercise the voting rights attached to the acquired securities before the Commission's decision approving the concentration.

The seriousness of an infringement of the standstill obligation is, of course, only the starting point when setting the fine. Indeed, in fixing the amount of the fine the Commission will take into account the possible additional factors of the gravity and also the duration of the infringement. Likewise, the Commission will also assess whether there are any mitigating and aggravating circumstances.

FTC

The standstill obligation is typically invoked under Section 7A of the Clayton Act, which is also known as the Hart-Scott-Rodino (HSR) Act. Section 7A prohibits certain mergers and acquisitions unless the parties have filed premerger notification reports with the Federal Trade Commission (FTC) and the Department of Justice (DOJ) and complied with the waiting period requirements.

BRAZIL

The standstill obligation arises from Article 88 of the Brazilian Competition Law (Law No. 12,529/2011). This provision prohibits the implementation of a concentration before it is analyzed and approved by the Administrative Council for Economic Defense (CADE), the country's competition authority. Violation of the standstill obligation can result in significant fines and other penalties.

CHINA

The standstill obligation is set out in Article 22 of the Anti-Monopoly Law (AML). This provision states that parties to a concentration must not implement the transaction before it has been notified to the State Administration for Market Regulation (SAMR) and has received clearance. The standstill obligation also applies during the review period set by SAMR, which can last up to 180 days.

FIRST PHASE AND SECOND PHASE INVESTIGATION

The provisions for the first phase and second phase investigation of mergers vary across jurisdictions.

INDIA

First Phase Investigation: In India, the first phase investigation is conducted by the Competition Commission of India (CCI). The CCI examines mergers that meet the thresholds specified in the Competition Act, which include turnover and asset thresholds. The CCI evaluates whether the

merger is likely to have a detrimental impact on competition in the relevant market. The parties are required to file a notice with the CCI containing information about the merger.

Second Phase Investigation: If the CCI has concerns about the merger's impact on competition, it can initiate a second phase investigation. During this phase, the CCI conducts a detailed examination of the merger, seeks information from market participants, and may require the parties to provide further information. The CCI may also consult with the parties to explore potential modifications to the transaction to address competition concerns. The second phase investigation can last up to 180 days.

UNITED STATES

First Phase Investigation: In the United States, the first phase investigation is typically conducted by the Federal Trade Commission (FTC) or the Department of Justice (DOJ) if the transaction meets the size thresholds under the Hart-Scott-Rodino (HSR) Act or if there are competitive concerns. During this phase, the FTC or DOJ reviews the merger to determine if there are potential anti-competitive effects. The parties are required to provide information and documents, and if concerns are identified, the FTC or DOJ may request additional information or negotiate remedies.

Second Phase Investigation: If the concerns raised during the first phase investigation are significant, the FTC or DOJ may initiate a second phase investigation. This phase involves more in-depth analysis and can lead to legal challenges or consent decrees. The second phase investigation is more time-consuming and has stricter deadlines compared to the first phase.

EUROPEAN UNION

First Phase Investigation: In the European Union (EU), the first phase investigation is initiated by the European Commission under the EU Merger Regulation (EUMR). The Commission examines mergers that have an EU dimension and meet the turnover thresholds. The Commission assesses whether the merger would significantly impede effective competition in the EU. The parties are required to submit a notification to the Commission with relevant information about the merger.

Second Phase Investigation: If the Commission has concerns about the merger's impact on competition, it can initiate a second phase investigation. This phase is more detailed and involves a more extensive review, including gathering information from the merging parties and third parties. The Commission can request remedies or modifications to address competition concerns, and the parties may propose remedies. The second phase investigation usually lasts up to 90 working days.

BRAZIL

CHINA

GREEN CHANNEL ROUTE

The Green Channel Route is an automated approval scheme which acts as a filter for certain kind of merger transaction or combination filings which don't possess any risk of harm to competition regimes. It is an automated approval system for combinations which will prove to be beneficial for parties falling into a certain category to avail the benefit of this scheme instead of waiting for a 30- day working period.

This route provides a bypass from the regular legal proceedings to enable them for speedy settlements and quicker administrative decisions. This also eliminates a mandatory 210 days period prescribed under the Act which CCI takes for an ex-ante investigation to see whether the transaction is causing any appreciable adverse effect on competition. For the sake of quicker disposal, parties are not required to mention market size, market share, competitor details etc. Thus, they are allowed for fewer disclosure requirements.

Procedure and eligibility criteria

The freshly inserted Schedule III of the amended combination regulations prescribes the methodology for parties to self-assess the proposed transaction by considering relevant market definitions in all cogent and reasonable ways and to determine whether the proposed transaction would be considered fit for Green Channel Approval or not. The self-assessing measure is stipulated so as to make entities understand the standpoint of each other and the possible economic & financial effects as a result of this transaction.

For parties to be considered fit for Green Channel approval, the below-mentioned points are to be fulfilled for proceeding further:

CCI received the first green Channel combination field under sub-section (2) of Section 6 of the Competition Act, 2002 (Act) read with regulations 5 and 5A of the Combination Regulations on 3rd October 2019. As on 20th July 2022, the total number of Green Channel notices received were 60, which accounted for about 25%.

Some Grey Areas in the Green Channel

The Guidance Notes provide clarity with respect to the word "complementary" which had been left undefined in the initial amendment. Citing the Canada Merger Enforcement Guidelines, CCI has said that complementary products are those which are related because they are combined and used together, do not compete with each other, and are not vertically related. An example given by the CCI is that of printers and ink cartridges. This definition, it is argued, is too wide and might prove to be problematic in certain sectors, like, automobile, where steering components could be seen as complementary to gear and seat products.

In addition to the above, the parties have to also supply information about their management- liaison, who knows the business well and will be engaging with the CCI. However, it is not clear as to how much flexibility will be allowed to the parties, in case of unavailability of the said liaison owing to valid and justified reasons.

INSOLVENCY AND BANKRUPTCY CODE

IBC provides for the framework for resolution of insolvency cases:

INDIA

IBC puts significant impact on the Competition commission of India. IBC allows for transfer of control of an insolvent company through corporate insolvency resolution. However, competition law requires that such transfer of control should not result in the abuse of dominance or anti- competitive practices.

For instance, if a potential buyer of an insolvent company is a dominant player in the market, the transfer of control may results in abuse of dominance.

In such a scenario, competition law may prevent the transfer of control of the insolvent company to the dominant player.

Settlement of debt can be another aspect of interface. IBC provides for settlement of debts in the course of insolvency proceedings. But, competition law requires that such settlement should not result in anti-competitive practices.

The interface can also be seen in the case of the liquidation of an insolvent company.

For instance, if the liquidation of an insolvent company results in the transfer of its assets to a dominant player in the market, such transfer may results in abuse of its dominant position, leads to anti competitive practices.

UNITED STATES

In the United States, competition law is primarily enforced by the Federal Trade Commission (FTC) and the Department of Justice (DOJ). The Hart-Scott-Rodino (HSR) Act and the Clayton Act are the key laws concerning competition.

Under the HSR Act, parties to a transaction meeting certain size thresholds must file premerger notification reports and observe a waiting period before completing the transaction. If the transaction raises competition concerns, the FTC or DOJ can file a lawsuit to block the merger or seek remedies, including divestitures.

When a company under bankruptcy protection files a motion to sell its assets, it may seek to invoke "Section 363 sales" as a means of expediting the sale process. In the context of competition law, the Section 363 motion can trigger concerns if the sale results in significant consolidation that may harm competition. The bankruptcy court has the authority to approve or reject such sales, taking into consideration competition concerns.

EUROPEAN UNION:

In the European Union (EU), competition law is enforced by the European Commission under the Treaty on the Functioning of the European Union (TFEU). The main regulation governing mergers is the EU Merger Regulation (EUMR).

In the context of insolvency proceedings, the EU merger control rules apply irrespective of the financial situation of the companies involved. There are no specific provisions that directly address the interface between the IBC and competition law. However, the European Commission has the authority to review and potentially block mergers under the EUMR if they would significantly impede effective competition in the EU.

CHINA:

In China, competition law is enforced by the State Administration for Market Regulation (SAMR). The Anti-Monopoly Law (AML) is the primary legislation governing competition.

In the context of insolvency proceedings, the AML applies to mergers and acquisitions involving companies under bankruptcy or reorganization. The SAMR must be notified of relevant transactions that exceed certain thresholds and undergo a merger review process. The SAMR can block or impose conditions on mergers that may harm competition.

BRAZIL:

In Brazil, competition law is enforced by the Administrative Council for Economic Defense (CADE) under Law No. 12,529/2011. The main regulation governing mergers is Resolution No. 2/2012.

CCI will endeavor to pass an order within 180 days from the date of notification. The Competition

Act provides for a deemed clearance if the CCI does not pass an order within 210 days from the date of notification.

Now it gets reduced to 150 days.

FTC:

Once the filing is complete, the parties must wait 30 days (15 days in the case of a cash tender offer or a bankruptcy) or until the agencies grant early termination of the waiting period before they can consummate the deal.

BRAZIL:

In Brazil, the time period for getting approval of a merger can vary depending on the specific circumstances of the transaction and the review process by the regulatory authority.

The regulatory authority responsible for overseeing mergers in Brazil is the Administrative Council for Economic Defense (CADE), which evaluates mergers for potential antitrust concerns

According to CADE's regulations, the approval process for mergers can take up to 240 days.

However, this timeframe is subject to certain conditions:

Additionally, parties to the merger can sometimes propose remedies or negotiate with CADE to expedite the process.

To ensure accuracy and up-to-date information, it is advisable to consult the specific regulations and guidelines provided by CADE or seek legal counsel familiar with the merger approval process in Brazil.

THRESHOLDS

The threshold limits for mergers to get approved by the authorities in Brazil, the United States, and China are as follows:

INDIA

Section 5 of the Competition Act sets out thresholds for enterprises and groups, in terms of assets and turnover, which if exceeded triggers a requirement to notify to the CCI.

EUROPEAN UNION

The threshold for notification to the European Commission is set out in Article 1(2) of the EU Merger Regulation (EUMR). This article states that a concentration must be notified if the following conditions are met:

BRAZIL

The threshold for the notification is established in Article 88 of the Brazilian Competition Law

In Brazil, mergers and acquisitions are subject to mandatory review by the Administrative Council for Economic Defense (CADE) if they meet certain turnover thresholds. Starting from January 2020, the mandatory notification applies to transactions in Brazil if:

UNITED STATES

In the United States, the Federal Trade Commission (FTC) and the Department of Justice (DOJ) are responsible for reviewing mergers for potential antitrust issues. The Hart-Scott-Rodino Antitrust Improvements Act (HSR Act) requires that parties to certain mergers and acquisitions above certain thresholds must file a premerger notification and observe a waiting period before completing the transaction. The HSR Act thresholds are revised annually and are currently set at

$92 million for 2022. Transactions valued above this threshold require a filing, but it's important to note that even transactions below this threshold may still be subject to review if certain other criteria are met.

The new thresholds are detailed in the chart below:

CHINA

The threshold for notification is provided in Article 21 of the Anti-Monopoly Law (AML).

In China, mergers and acquisitions are subject to review by the State Administration for Market Regulation (SAMR) under the Anti-Monopoly Law (AML). The AML requires mandatory

notification of concentrations if the combined worldwide turnover of all undertakings involved in the concentration in the previous fiscal year exceeds CNY 10 billion ($1.5 billion), and at least two of the undertakings involved have generated each at least CNY 400 million ($61 million) in China in the previous fiscal year. There are also separate rules for mergers involving financial institutions.

SAMR's draft Notification Thresholds Rules will amend China's mandatory notification thresholds as follows:

Acquisition, merger or amalgamation, if the enterprise being acquired, taken control of, merged or amalgamated has (i) assets less than INR 350crore, or (ii) turnover less than INR 1000crore. This exemption is valid for a period of 5 years from the date of publication of its notification in the official gazette. The de-minimus has been extended by Central Government for a further 5 years period vides notification dated 16th March 2022. Section 44 and 45 of the Act, 2002

In case any party either makes a false statement or omits to state any material facts then a penalty of INR 1crore can be imposed under section 44 of the Act. Similarly, section 45 of the act prescribes a penalty up to INR 1crore on any person who makes false statements or omits to state any material facts, knowing it to material or willfully alters, suppresses or destroys any document which is required to be furnished. Sub section (2) of section 45 also empowers CCI to pass "such orders as it deems fit".

UNITED STATES In the United States, there is no specific de minimis threshold for mergers. The Hart-Scott-Rodino (HSR) Act requires parties to certain mergers and acquisitions above a certain dollar threshold to file a premerger notification and observe a waiting period. For 2022, the HSR Act threshold is $92 million. Transactions below this threshold are not subject to the HSR Act filing requirement, but they may still be subject to review if other criteria are met.

BRAZIL In Brazil, there is no specific de minimis threshold for mergers. However, as mentioned earlier, mergers and acquisitions are subject to mandatory review by the Administrative Council for Economic Defense (CADE) if they meet turnover thresholds. The current turnover thresholds are BRL 750 million (approximately USD 143 million) for at least one party involved and BRL 75 million (approximately USD 14.3 million) for at least one other party involved.

EUROPEAN UNION In the European Union, the de minimis threshold for mergers is determined by the EU Merger Regulation. Under this regulation, transactions must be notified to the European Commission if certain turnover thresholds are exceeded. Currently, if the combined worldwide turnover of the merging companies exceeds EUR 5 billion, and each of at least two of the companies involved has an EU-wide turnover of at least EUR 250 million, then the merger must be notified to the European Commission.

CHINA In China, the de minimis threshold for mergers is set under the Anti-Monopoly Law (AML). As mentioned earlier, mandatory notification is required if the combined worldwide turnover of all undertakings involved in the concentration in the previous fiscal year exceeds CNY 10 billion ($1.5 billion), and at least two of the undertakings involved have generated each at least CNY 400 million ($61 million) in China in the previous fiscal year.

REFERENCES

Statutes:

Most countries in the world have enacted competition laws to protect their free market economies and have thereby developed an economic system in which the allocation of resources is determined solely by demand and supply. In the case of India, the earlier Monopolies and Restrictive Trade Practices Act, 1969 (MRTP) was not only found to be inadequate but also obsolete in certain respects, particularly, in the light of such international economic developments relating to competition law.

To overcome such difficulty Indian Government has enacted the Competition Act in 2002. This enactment is seen as India's response to the opening up of its economy, removing controls and resorting to liberalization. The Act sought to ensure fair competition in India by prohibiting trade practices which cause appreciable adverse effect on the competition in market within India.

The present Indian Act is quite contemporary to the laws presently in force in the European Community as well as in the United Kingdom or in any other jurisdictions. In other words, the laws dealing with competition in these jurisdictions have somewhat similar legislative intent and scheme of enforcement.

We are living in a free market economy age where business entities are engaged in practicing competition. Sometimes it leads to the monopolization of market by way of anti-competitive agreements, abuse of dominance, mergers and takeovers between business entities which results in distortion of market. Most countries in the world have enacted competition laws to protect their free market economies and have thereby developed an economic system in which the allocation of resources is determined solely by demand and supply.

In the case of India, the earlier Monopolies and Restrictive Trade Practices Act, 1969 (MRTP) was not only found to be inadequate but also obsolete in certain respects, particularly, in the light of such international economic developments relating to competition law. To overcome such difficulty Indian Government has enacted the Competition Act in 2002. This enactment is seen as India's response to the opening up of its economy, removing controls and resorting to liberalization.

The Act sought to ensure fair competition in India by prohibiting trade practices which cause appreciable adverse effect on the competition in market within India. The present Indian Act is quite contemporary to the laws presently in force in the European Community as well as in the United Kingdom or in any other jurisdictions. In other words, the laws dealing with competition in these jurisdictions have somewhat similar legislative intent and scheme of enforcement.

Historical background of merger

The concept of merger and acquisition in India was not popular until the year 1988. During that period a very small percentage of businesses in the country used to come together, mostly into a friendly acquisition with a negotiated deal. The key factor contributing to fewer companies involved in the merger was the regulatory and prohibitory provisions of MRTP Act, 1969. According to this Act, a company or a firm has to follow a burdensome procedure to get approval for merger and acquisitions.

The year 1988 witnessed one of the oldest business acquisitions or company mergers attempt in India.

It is the well-known ineffective unfriendly takeover bid by Swaraj Paul to overpower DCM Ltd. and Escorts Ltd. Further to that many other non-resident Indians had put in their efforts to take control over various companies through their stock exchange portfolio.

Before 1991 Indian economy was closed economy. Various licenses and registration under various enactments were required to set-up an industry. Due to restrictive government policies and rigid regulatory framework there existed very limited scope for restructuring.

However after 1991, the main thrust of industrial policy 1991, was on relaxations in industrial licensing, foreign investments, and transfer of foreign technology, etc. With the economic liberalization, globalization and opening-up of economies, the Indian corporate sector started restructuring businesses to meet the opportunities and challenges.

Regulatory approval of schemes

- The merger and takeover involves various issues and compliance not even of the

Companies Act, 2013, but from the other Regulators also depending upon the

nature of business of the company and sector under which it is operating. These

may include SEBI, RBI, CCI, Stock Exchanges, IRDAI, TRAI, etc.

- The Companies Act, 2013 requires that notice of the Merger be sent along with

such other documents as the Scheme and valuation report, not only to

shareholders and creditors, but also to various regulators like the Ministry of

Corporate Affairs, the Reserve Bank of India (in cases, where non-resident

investors are involved),

- SEBI and Stock Exchanges (for listed companies), Competition Commission of India

(in cases where the prescribed fiscal thresholds are being crossed and the

proposed merger could have an adverse effect on competition), Income Tax

authorities and any other relevant industry regulators or authorities which are

likely to be affected by the merger.

- This ensures compliance of the Scheme with any and all other regulatory and

statutory requirements that need to be followed by the merging entities.

Combination (Section 5 of Competition Act, 2002)

The Competition Act 2002 is the principal legislation that regulates combinations (acquisitions, mergers, amalgamations and de-mergers) in India. Sections 5 and 6 of the Competition Act, which deal with the regulation of combinations, have been in force since 1st June 2011. Prior to this date there was no statutory obligation to notify to any antitrust authority before completing merger and amalgamations. Section 5 of the Act prescribes the jurisdictional thresholds limits (based on asset and turnover of combining companies) for transactions that must be notified to CCI prior to implementation of merger and acquisition.

Meaning of combination for the purpose of Competition Act

- Any acquisition, merger or amalgamation that meets the following jurisdictional thresholds limits, as provided in Section 5 of the Competition Act, 2002, is a "combination" for the purpose of the Act.

- The thresholds relate to the assets and turnover of the parties to the combination, i.e., target enterprise and acquirer (or acquirer group) / merging parties (or the group to which merged entity would belong).

- If the jurisdictional thresholds are met and exemptions are unavailable, it is mandatory to notify the Competition Commission of India (CCI) of the combination. Approval of CCI is must.

- CCI will consider whether proposed Combination is having any appreciable adverse impact on competition in India or not.

Regulatory Authority for Notifying Combinations- The Competition Commission of India (CCI) is the statutory authority responsible for reviewing combinations and assessing whether or not they cause or are likely to cause an appreciable adverse effect on competition within the relevant market(s) in India. CCI approval is required for combinations where the parties involved exceed the assets/turnover thresholds set out in section 5 of the Competition Act.

Exemption from provision of Combination

The Central govt. has granted exemption from application of section 5 or Section 6:

- To the enterprise being party to any acquisition or where enterprises whose control, shares, voting rights or assets are being acquired, having assets of the value of not more than 350crores or turnover of not more than 1000crore from the combination provision of the act for 5 years.

- To public interest all cases of reconstitution, transfer of undertaking or amalgamation banking companies as per Banking Acts for a period of 10 years

- In public interest to the Regional Rural banks for a period of 5 years

- To Central Public Sector Enterprises (CPSES) engaged in the Oil and Gas Sectors (OGS) along with their wholly or partly owned subsidiaries operating in OGS for a period of 5 years.

- Any one of the following events requires approval of Regulatory Authority:

- The acquisition of:

- Shares

- Voting rights

- Assets

- Control in one or more enterprises

Types of notifiable transactions:

Section 5 of the Competition Act, 2002 covers three broad categories of combinations:

- The acquisition by one or more persons of control, shares, voting rights, or assets of one or more enterprises, where the parties, or the group to which the target will belong post-acquisition, meet the specified assets/turnover thresholds.

- The acquisition by a person of control over an enterprise where the person concerned already has direct and indirect control over another enterprise with which it competes, where the parties, or the group to which the target will belong post-acquisition, meet the specified assets/turnover thresholds.

- Mergers or amalgamations, where the enterprise remaining, or enterprise created, or the group to which the enterprise will belong after the merger/amalgamation, meets the specified assets/turnover thresholds.

- The Combination Regulations provide that the CCI will "Endeavour" to pass an order or issue directions within a period of 180 days from the date of notification. The Competition Act provides for a deemed clearance if the CCI does not pass an order within 210 days from the date of notification.

- No person or enterprise shall enter into a combination which causes or is likely to cause an appreciable adverse effect on competition within the relevant market in India, and such a combination shall be void.

- Subject to the provisions contained in sub-section (1), any person or enterprise, who or which proposes to enter into a combination, shall give notice to the Commission, in the form as may be specified, and the fee which may be determined, by regulations, disclosing the details of the proposed combination, within thirty days of

- Approval of the proposal relating to merger or amalgamation, referred to in clause (c) of section 5 by the board of directors of the enterprises concerned with such merger or amalgamation, as the case may be;

- Execution of any agreement or other document for acquisition referred to in clause (a) of section 5 or acquiring of control referred to in clause (b) of that section.

Taxation aspects of Merger and Amalgamation

The word 'amalgamation' or 'merger' is not defined anywhere in the Companies Act, 1956. However, the Companies Act, 2013 without strictly defining the term explains the concept. A 'merger' is a combination of two or more entities into one; the desired effect being not just the accumulation of assets and liabilities of the distinct entities, but organization of such entity into one business. Section 2(1B) of the Income Tax Act, 1961 defines the term 'amalgamation' as follows:

"Amalgamation" in relation to companies, means the merger of one or more companies with another company or the merger of two or more companies to form one company (the company or

companies which so merge being referred to as the amalgamating company or companies and the company with which they merge or which is formed as a result of the merger, as the amalgamated company), in such a manner that:

- All the property of the amalgamating company or companies immediately before the amalgamation becomes the property of the amalgamated company by virtue of the amalgamation.

- All the liabilities of the amalgamating company or companies immediately before the amalgamation become the liabilities of the amalgamated company by virtue of the amalgamation.

- shareholders holding not less than three-fourths in value of the shares in the amalgamating company or companies (other than shares already held therein immediately before the amalgamation by, or by a nominee for, the amalgamated company or its subsidiary) become shareholders of the amalgamated company by virtue of the amalgamation, otherwise than as a result of the acquisition of the property of one company by another company pursuant to the purchase of such property by the other company or as a result of the distribution of such property to the other company after the winding up of the first mentioned company.

Stamp duty aspects of Merger and Amalgamation:

- Stamp duty is a duty payable on certain specified instruments/documents. Broadly speaking, when there is a conveyance or transfer of any movable or immovable property, the instrument or document affecting the transfer is liable to payment of stamp duty.

- Stamp duty on court order for mergers/demergers- Since the order of the Court merging two or more companies, or approving a demerger, has the effect of transferring property to the surviving /resulting company, the order of the NCLT may be required to be stamped. The stamp laws of most states require the stamping of such orders. The amount of the stamp duty payable would depend on the state specific stamp law.

Federal Trade Commission (FTC) - United States:

In the United States, the FTC, along with the Department of Justice, enforces antitrust laws, including the Hart-Scott-Rodino (HSR) Act. Among the key provisions in U.S. antitrust law is one designed to prevent anticompetitive mergers or acquisitions. Under the Hart-Scott-Rodino Act, the FTC and the Department of Justice review most of the proposed transactions that affect commerce in the United States and are over a certain size, and either agency can take legal action to block deals that it believes would "substantially lessen competition." Although there are some exemptions, for the most part current law requires companies to report any deal that is valued at more than $101 million to the agencies so they can be reviewed.

Steps in the Merger Review Process:

- Filing notice of a proposed deal:

- Once the filing is complete, the parties must wait 30 days (15 days in the case of a cash tender offer or a bankruptcy) or until the agencies grant early termination of the waiting period before they can consummate the deal.

- Clearance to one antitrust agency:

- Parties proposing a deal file with both the FTC and DOJ, but only one antitrust agency will review the proposed merger. Staffs from the FTC and DOJ consult and the matter is "cleared" to one agency or the other for review (this is known as the "clearance process"). Once clearance is granted, the investigating agency can obtain non-public information from various sources, including the parties to the deal or other industry participants.

- Waiting period expires or agency issued second notice:

- After a preliminary review of the premerger filing, the agency can:

- Terminating the waiting period prior to the end of the waiting period

- Allow initial waiting period to expire

- Issue a request for additional information

- Parties substantially comprise with the second request:

- Typically, once both companies have substantially complied with the Second Request, the agency has an additional 30 days to review the materials and take action, if necessary. (In the case of a cash tender offer or bankruptcy, the agency has 10 days to complete its review and the time begins to run as soon as the buyer has substantially complied.) The length of time for this phase of review may be extended by agreement between the parties and the government in an effort to resolve any remaining issues without litigation.

- The waiting period expires or the Agency challenges the deal:

- The potential outcomes at this stage are:

- Close the investigation and let the deal go forward unchallenged;

- Enter into a negotiated consent agreement with the companies that includes provisions that will restore competition; or

- Seek to stop the entire transaction by filing for a preliminary injunction in federal court pending an administrative trial on the merits.

Clearance to one antitrust agency:

Parties proposing a deal file with both the FTC and DOJ, but only one antitrust agency will review the proposed merger. Staffs from the FTC and DOJ consult and the matter is "cleared" to one agency or the other for review (this is known as the "clearance process"). Once clearance is granted, the investigating agency can obtain non-public information from various sources, including the parties to the deal or other industry participants.

Waiting period expires or agency issued second notice

After a preliminary review of the premerger filing, the agency can:

- Terminating the waiting period prior to the end of the waiting period

- Allow initial waiting period to expire

- Issue a request for additional information

Typically, once both companies have substantially complied with the Second Request, the agency has an additional 30 days to review the materials and take action, if necessary. (In the case of a cash tender offer or bankruptcy, the agency has 10 days to complete its review and the time begins to run as soon as the buyer has substantially complied.) The length of time for this phase of review may be extended by agreement between the parties and the government in an effort to resolve any remaining issues without litigation.

- The waiting period expires or the Agency challenges the deal

- Close the investigation and let the deal go forward unchallenged;

- Enter into a negotiated consent agreement with the companies that includes provisions that will restore competition; or

- Seek to stop the entire transaction by filing for a preliminary injunction in federal court pending an administrative trial on the merits.

The FTC conducts a thorough investigation to determine if the merger would substantially lessen competition. Factors Considered:

The FTC considers market concentration, entry barriers, potential efficiencies, and other factors to assess competitive impact Remedies:

The FTC may seek remedies, such as divestitures or behavioral remedies, to address anticompetitive concerns.

EUROPEAN UNION:

The development of merger control in the European Union

The European Union ("the EU") is a regional grouping of (at the time of writing) 25 European States. It is based on a number of international treaties of which the most important, for present purposes, is the Treaty establishing the European Community ("the EC Treaty"). The Member States of the European Community (the EC) are the same as the Member States of the EU. The difference between the EU and the EC is largely technical and not relevant in the present context. No specific provision is made for the control of mergers in the EC Treaty.

The main competition rules contained in the Treaty, Articles 81 and 82 EC, are primarily directed at controlling the conduct of firms (or "undertakings") rather than at changes to the structure of the market. Neither explicitly mentions mergers. Despite the creative interpretation of Articles 81 and 82 EC, which extended their application to at least some merger activity, it was apparent from an early stage in the EC's development that legislation would be needed in order to institute an effective system of merger control.

The Commission of the European Communities ("the Commission") first proposed a regulation on the subject in 1973. It was not until 1989, however, that agreement could finally be reached among the Member States. The result was the adoption of Council Regulation (EEC) No. 4064/89, which was subsequently amended in 1997, and was replaced in 2004 by a new Regulation No. 139/2004, further modifying and consolidating the EC system of merger control.

The attempt to use Articles 81 and 82 EC to control mergers